News Summary

Niva Bupa Health Insurance has emerged as a prominent player in India’s health insurance market, especially in the family mediclaim segment. This Niva Bupa review examines what customers receive, what gaps remain, and how pricing compares in a competitive and rapidly evolving insurance landscape. With rising healthcare costs and growing awareness around financial protection, family health insurance plans have become essential for Indian households.

The Niva Bupa family health insurance plans offer comprehensive coverage, including hospitalization expenses, cashless treatment across a wide hospital network, and add-on benefits such as maternity and critical illness coverage. The company emphasizes a cashless claims process and quick approvals, which appeal to urban and semi-urban customers. At the same time, policyholders must consider exclusions, waiting periods, and premium costs before choosing a plan.

Industry reports suggest that India’s health insurance sector is expanding due to increased healthcare inflation, digital adoption, and regulatory push toward insurance penetration. As a result, companies like Niva Bupa are investing in technology, customer experience, and product innovation to stay competitive. However, challenges such as claim rejections, pricing transparency, and policy complexity remain concerns across the sector.

This detailed Niva Bupa family health insurance review explores the company’s background, business model, product offerings, costs, and limitations. It also compares the company’s position within the broader insurtech and fintech ecosystem, helping readers understand whether these plans meet modern healthcare needs.

1. Understanding Niva Bupa and Its Market Position

1.1 What is Niva Bupa?

Niva Bupa Health Insurance operates in a space where decisions are rarely logical alone. Health insurance, for most Indian families, is an emotional purchase. It is not just about saving money. It is about protecting dignity when things go wrong. Niva Bupa began its journey as Max Bupa. The rebranding was more than a name change. It marked a shift toward becoming a more agile, consumer-focused company in a market that was rapidly digitizing.

Today, the company positions itself as digital-first. That sounds like a buzzword, but it has real implications. Buying a policy can take minutes instead of days. Claims can be tracked on a phone instead of through endless calls. Documents are uploaded, not couriered. For a young family buying insurance for the first time, this feels empowering. For older customers, it can feel slightly overwhelming. That contrast defines much of Niva Bupa’s experience. At its core, the company is trying to simplify something that has always felt intimidating. It does not always succeed perfectly. But the intent is visible in how its products and processes are designed.

1.2 Founders, Ownership, and Background

Niva Bupa is a joint venture between India’s Max Group and the UK-based healthcare giant Bupa. This partnership is not just structural. It deeply influences how the company operates. Bupa brings decades of global experience in healthcare systems. It understands risk, claims behavior, and long-term sustainability. Max Group brings local insight. It understands how Indian families think about money, health, and trust. This combination shows up in subtle ways. Policies are structured with discipline. Processes follow defined frameworks. At the same time, the company tries to adapt to Indian realities, where documentation can be inconsistent and medical access varies widely.

For customers, this means dealing with a company that feels more organized than many local insurers. However, it also means that rules are enforced with clarity. Claims are not emotional decisions. They are process-driven. That gap between expectation and reality is where many customer experiences are shaped.

1.3 Growth in the Indian Startup Ecosystem

Even though Niva Bupa is not a startup, it behaves like one in important ways. It has embraced digital platforms, invested in user experience, and tried to remove friction from insurance buying. In India, insurtech startups have pushed the industry to evolve faster. Customers now expect instant responses, simple interfaces, and transparent pricing. Niva Bupa has clearly responded to this shift.

Its apps, online policy issuance, and digital claims tracking reflect this change. For a generation that prefers doing everything on a phone, this matters. However, growth in insurance is not like growth in e-commerce. You do not measure success by downloads or sign-ups. You measure it by trust built over time. Every claim settled smoothly builds confidence. Every delay or rejection creates doubt. Niva Bupa’s growth story sits right in the middle of this balance. It is modern in approach, but it still operates in a sector where human trust matters more than technology.

2. Niva Bupa Family Health Insurance Plans Explained

2.1 Overview of Family Mediclaim Policies

Family mediclaim plans are often bought during moments of realization. A hospital visit, a rising bill, or even a friend’s experience can trigger the decision. Under a single policy, multiple family members are covered. This includes spouses, children, and sometimes parents. Instead of managing separate policies, everything is consolidated. Niva Bupa Health Insurance offers these plans with flexible coverage amounts. You can choose how much financial protection you want.

In practical life, this flexibility matters. A young couple may choose a modest cover. A family with elderly parents may opt for a higher sum insured. But there is a trade-off. Since the coverage is shared, one major hospitalization can reduce the remaining amount available for others. This is where real-life decisions become difficult. Insurance is not just a product. It is a silent agreement within a family about risk and responsibility.

2.2 Key Features of Niva Bupa Plans

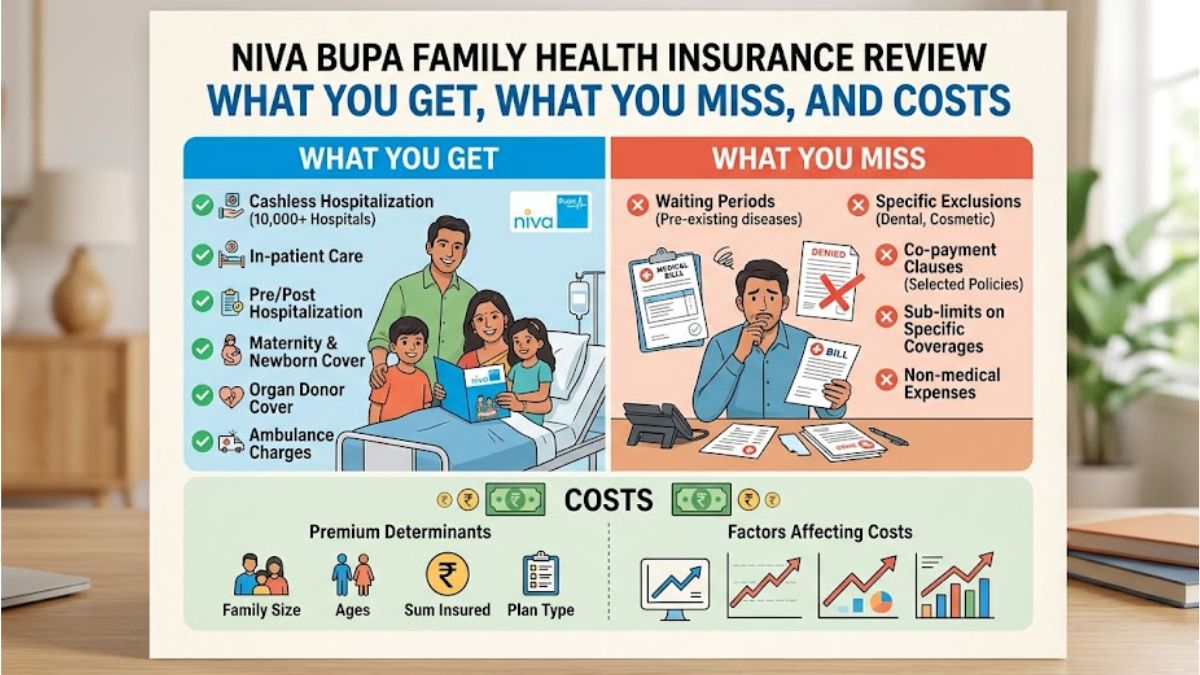

On paper, Niva Bupa’s plans look comprehensive. But the real question is how these features play out when someone actually needs them. Cashless hospitalization is one of the biggest advantages. Imagine rushing a family member to the hospital. In that moment, arranging money is the last thing you want to worry about. If the hospital is part of the network, the insurer settles the bill directly. This can ease a lot of stress. However, approval is not always instant. Sometimes, families still feel anxious while waiting.

Pre and post hospitalization coverage is another important feature. Medical expenses rarely begin at admission. Tests, consultations, and medicines start earlier and continue after discharge. Many people underestimate these costs. Having them covered makes a real difference over time. Daycare procedures reflect modern healthcare. Treatments that once required days in a hospital can now be completed within hours. Covering these procedures shows that the policy is aligned with current medical practices. Ambulance charges may seem minor. But in emergencies, every cost feels heavy. Including them adds completeness to the plan. Still, features alone do not define value. The experience during a claim does.

2.3 Cashless Network and Accessibility

The idea of a wide hospital network sounds reassuring. And in many cases, it truly is. With Niva Bupa, policyholders can access a large number of hospitals for cashless treatment. This reduces the need to arrange large sums of money upfront. When everything works smoothly, the experience feels almost effortless. You focus on the patient, not the bill. But real experiences can vary. Some customers report seamless claims, where approvals come quickly and billing is handled efficiently.

Others face delays. Documents may be requested multiple times. Communication between the hospital and insurer may slow things down. These moments matter. They shape how people remember the brand. Insurance is not tested when you buy it. It is tested when you use it. Niva Bupa has clearly invested in improving this experience through digital tools and faster processing systems. Yet, like most insurers in India, the final experience often depends on coordination between multiple parties. In the end, accessibility is not just about how many hospitals are listed. It is about how supported a family feels during a crisis.

3. What You Get: Benefits and Coverage

3.1 Hospitalization and Treatment Coverage

At its core, a health insurance plan is about covering hospitalization costs. Niva Bupa does this in a structured and fairly comprehensive way. Expenses such as room rent, doctor fees, surgical costs, and ICU charges are typically included. For many families, this forms the backbone of financial protection. A single hospitalization can cost lakhs. Without insurance, this can disrupt savings built over years.

With coverage in place, the financial burden reduces significantly. But it is important to understand limits. Room rent caps or sub-limits can affect how much is actually reimbursed. This is where many customers feel caught off guard. The policy covers the event, but not always the full cost. Understanding these nuances before buying makes a big difference later.

3.2 Additional Benefits and Riders

Insurance is no longer just about basic hospitalization. Customers now expect more flexibility and customization. Niva Bupa offers add-ons like maternity coverage and critical illness riders. These options allow families to tailor the policy to their needs. For a young couple planning a family, maternity coverage can be valuable. For someone concerned about serious illnesses, a critical illness rider provides an extra safety net.

But these benefits come at a cost. Premiums increase as you add more coverage. This creates a common dilemma. Should you pay more now for broader protection, or keep premiums low and risk higher out-of-pocket costs later? There is no universal answer. It depends on personal priorities, financial comfort, and risk perception.

3.3 Wellness and Preventive Care

One of the more interesting shifts in modern insurance is the focus on prevention. Niva Bupa promotes wellness programs that encourage healthier lifestyles. This may include health check-ups, fitness tracking, or rewards for maintaining good health. At first glance, these features may seem secondary. But over time, they can influence behavior. Instead of only reacting to illness, the idea is to reduce the chances of getting sick in the first place.

For customers, this creates a different relationship with insurance. It is no longer just a safety net. It becomes a partner in maintaining health. However, the effectiveness of these programs depends on engagement. Many users ignore them after purchase. The real value lies in consistently using these tools. And that requires a mindset shift, not just a product feature.

4. What You Miss: Limitations and Exclusions

4.1 Waiting Periods and Exclusions

No matter how promising a policy looks, there is always a layer that people only discover later. With Niva Bupa Health Insurance, like most insurers, that layer comes in the form of waiting periods and exclusions. At the time of purchase, everything feels reassuring. You believe you are covered. But when a medical need arises early, reality can feel different. Certain illnesses, especially pre-existing conditions, are not covered immediately. You may need to wait months or even years before the policy fully protects you.

For a healthy person, this might seem like a small detail. But for someone who buys insurance after a health scare, this waiting period can feel frustrating. It creates a gap between expectation and actual support. Exclusions are another area that often goes unnoticed. Some treatments, conditions, or procedures may never be covered. These are written clearly in documents, but rarely read with full attention. This is not unique to Niva Bupa. It is how the entire insurance system works. Still, for customers, the emotional impact is real. You only understand these limits when you need the policy the most.

4.2 Policy Complexity

Insurance documents are not written for comfort. They are written for precision. And that often makes them difficult to understand. Niva Bupa has tried to simplify communication. Yet, the reality is that policy wordings still require careful reading. Terms like sub-limits, co-payments, and exclusions can confuse even well-informed buyers. Many customers rely on agents or online summaries. They assume they understand the policy. But when a claim happens, small details suddenly become very important.

A room rent limit, for example, can quietly affect the total claim amount. If the hospital room exceeds the allowed category, other expenses may be proportionately reduced. This is where frustration builds. Customers feel they were not informed clearly, while insurers rely on documented terms. The gap is not always about intent. It is about interpretation. To truly benefit from a policy, one must go beyond the brochure. It requires patience, attention, and sometimes uncomfortable questions before buying.

4.3 Premium Costs and Affordability

Health insurance always feels affordable until you start customizing it. At a basic level, Niva Bupa offers competitive premiums. But as you add higher coverage, include older family members, or choose add-ons, the cost rises quickly. For a young individual, premiums may feel manageable. But for a family with aging parents, the numbers can become significant. This creates a real dilemma. Do you reduce coverage to save money? Or do you pay more for better protection?

For many middle-class families, this decision is not easy. Insurance competes with other financial priorities like education, housing, and daily expenses. There is also the emotional aspect. Paying premiums year after year without making a claim can feel like a loss. Yet, skipping insurance can be far more expensive during a medical emergency. Affordability, therefore, is not just about price. It is about perceived value and long-term thinking.

5. Pricing and Cost Analysis of Niva Bupa Plans

5.1 Factors Affecting Premiums

Premium calculation in health insurance is not random. It reflects risk, and risk is deeply personal. With Niva Bupa Health Insurance, factors like age play a major role. A younger person pays less because the probability of claims is lower. As age increases, premiums rise sharply. Health condition is another critical factor. Pre-existing diseases, lifestyle habits, and medical history influence pricing.

Location also matters more than people realize. Healthcare costs differ across cities. Living in a metro can lead to higher premiums due to higher treatment expenses. Even lifestyle choices quietly affect pricing. Smoking, for instance, increases risk and therefore cost. All these variables combine to create a premium that feels personal. Two families with similar structures may still pay very different amounts.

5.2 Cost vs Value Proposition

The real question is not how much you pay. It is what you get in return. Niva Bupa often positions itself as offering strong value for money. Its plans include wide coverage, a large hospital network, and digital convenience. For some customers, this balance works well. They feel secure knowing that major expenses are covered and claims can be processed smoothly.

For others, the value becomes questionable if they face claim issues or discover limitations later. Value in insurance is not fixed. It depends on how closely the policy matches your needs. A plan that works perfectly for one family may feel inadequate for another. This is why comparison alone is not enough. Understanding your own risks is more important.

5.3 Hidden Costs and Considerations

The price you see is not always the price you pay. Co-payments are one such factor. In some cases, the policyholder must pay a portion of the claim amount. This reduces the insurer’s liability but increases out-of-pocket expenses. Deductibles work in a similar way. You agree to pay a certain amount before the insurance kicks in.

These conditions are not necessarily negative. They often help reduce premiums. But they must be understood clearly. There are also indirect costs. Choosing a hospital outside the network can lead to reimbursement delays. Opting for higher room categories can increase personal expenses. Transparency becomes crucial here. A well-informed customer is less likely to feel disappointed later. Insurance is not just about buying a policy. It is about understanding how it behaves under pressure.

6. Business Model and Revenue Strategy

6.1 How Niva Bupa Operates

At its core, Niva Bupa Health Insurance follows a traditional insurance model. It collects premiums from policyholders and uses that pool to pay claims. This system works on probability. Not everyone will claim at the same time. The company relies on this balance to remain financially stable. However, the simplicity of this model hides a complex backend. Risk assessment, underwriting, and claim evaluation require constant analysis. From a customer’s perspective, the process feels straightforward. You pay regularly and expect support when needed. From the company’s side, every policy issued is a calculated decision.

6.2 Revenue Streams

Premiums form the primary source of revenue. This is the backbone of the business. But that is not the only income stream. The company also invests collected funds in financial instruments. These investments generate returns, adding to overall profitability. Partnerships also play a role. Tie-ups with hospitals, aggregators, and digital platforms expand reach and drive policy sales. This multi-layered revenue model ensures stability. It allows the company to manage risk while continuing to grow.

6.3 Role of Technology

Technology is no longer optional in insurance. It defines the experience. Niva Bupa has invested heavily in digital platforms. From buying policies online to tracking claims through apps, the process has become faster and more transparent. For customers, this reduces friction. You no longer need to visit offices or handle physical paperwork for most tasks. Behind the scenes, technology also improves efficiency. Data analytics helps in risk assessment. Automation speeds up claims processing. This shift reflects a larger transformation in the industry. Insurance is no longer just a financial product. It is becoming a digital service.

7. Industry Trends and Growth of Health Insurance in India

7.1 Rising Healthcare Costs

Healthcare in India is becoming more expensive every year. A single hospitalization can wipe out years of savings. This reality is pushing more families toward insurance. People are no longer viewing health insurance as optional. It is becoming a necessity. The rising cost of treatment is the biggest driver behind this shift.

7.2 Increasing Insurance Penetration

Awareness around health insurance has grown significantly. More people now understand the risks of being uninsured. This is especially true after recent global health crises. As a result, the number of insured families is increasing. Companies like Niva Bupa Health Insurance are benefiting from this trend. However, penetration is still low compared to developed markets. This means there is significant room for growth.

7.3 Role of Fintech and Insurtech

The insurance industry is changing faster than ever. Companies are using artificial intelligence and data analytics to improve decision-making. This helps in faster claims processing and better risk evaluation. Customer engagement is also evolving. Digital platforms, apps, and personalized communication are becoming standard. For customers, this means quicker responses and more control. For companies, it means higher efficiency and scalability. This transformation is not just about technology. It is about redefining how insurance fits into everyday life.

8. Competitors and Market Comparison

8.1 Direct Competitors

When you look at Niva Bupa Health Insurance in isolation, the plans may seem comprehensive. But the real clarity comes when you place it next to its competitors. Companies like Star Health and Allied Insurance operate in the same space and target similar customers. They offer family mediclaim policies with comparable coverage, hospital networks, and claim structures. On the surface, the differences feel small. Sum insured options look similar. Benefits overlap. Pricing often falls within a comparable range.

But when you go deeper, the differences start to matter. Some insurers are known for faster claim settlements. Others have stronger hospital tie-ups in certain regions. A few offer slightly more flexible terms for older customers. From a real customer’s perspective, these nuances are everything. You do not feel the difference when buying the policy. You feel it when you are sitting in a hospital, waiting for approval. That is where competition becomes real. It is no longer about brochures. It is about who delivers when it truly matters.

8.2 Indirect Competitors

Interestingly, some of the biggest influences on your decision are not insurers at all. Platforms like Policybazaar have quietly changed how people buy insurance. They do not sell just one company’s product. They show multiple options side by side. For a customer, this creates both clarity and confusion.

On one hand, you can compare premiums, features, and coverage in minutes. On the other hand, too many options can feel overwhelming. Every plan looks good in isolation. These platforms also shape perception. A plan with better ratings or more visibility often gets more attention, even if the difference is marginal. In many cases, the final decision is influenced not just by the insurer, but by how the plan is presented and explained. This makes aggregators powerful indirect competitors. They control the first impression, and in insurance, first impressions matter more than we admit.

8.3 Competitive Advantage

Niva Bupa’s biggest strength lies in how it tries to make the experience feel less intimidating. Its digital-first approach is not just about convenience. It is about control. Customers can explore plans, understand features, and track claims without feeling dependent on agents. For a younger audience, this feels natural. Everything happens on a screen. The process feels fast, almost effortless.

For older customers, however, the experience can feel slightly distant. They may still prefer human interaction and reassurance. What Niva Bupa is trying to do is bridge this gap. It wants to combine the efficiency of technology with the trust of traditional service. When it works, the experience feels smooth and modern. When it does not, customers feel the absence of human support more strongly. That balance is where its true competitive advantage will either strengthen or weaken over time.

9. Customer Experience and Claims Process

9.1 Ease of Buying Policies

Buying insurance used to be a slow, paperwork-heavy process. It involved agents, forms, and waiting periods. With Niva Bupa Health Insurance, that experience has changed significantly. You can now browse plans online, compare options, and complete the purchase within minutes. The process feels simple, almost like buying any other digital product. For many first-time buyers, this ease removes a major barrier. There is no pressure from agents. No rush to decide. You move at your own pace.

But simplicity has its downside. When everything feels easy, people sometimes skip the deeper reading. They rely on summaries instead of understanding full terms. This creates a silent risk. The buying experience is smooth, but the understanding may not be complete. And in insurance, what you do not understand can matter more than what you do.

9.2 Claims Settlement Process

The real test of any insurance policy is not how it is sold. It is how it responds when you need it. Niva Bupa offers a cashless claims process. In ideal conditions, this means the hospital coordinates directly with the insurer, and you do not have to pay upfront. When this works well, it feels like a huge relief. Families can focus on the patient instead of finances. But real experiences vary.

Some customers report quick approvals and seamless processing. Everything happens quietly in the background. Bills are settled without stress. Others face delays. Documents may be requested multiple times. Approvals can take longer than expected. These moments are emotionally intense. You are already dealing with a medical situation. Any uncertainty around money adds pressure. The claims process, therefore, is not just operational. It is deeply emotional. It defines how customers remember the brand long after the treatment is over.

9.3 Customer Feedback Trends

Customer feedback around Niva Bupa reflects a mix of satisfaction and frustration. On one side, many users appreciate the ease of purchase, the digital interface, and the availability of cashless treatment. They feel the company has simplified a traditionally complex process. On the other side, there are concerns. Some customers talk about delays in claims or confusion around policy terms.

What is important to understand is that insurance feedback is rarely neutral. Experiences are shaped during high-stress situations. A smooth claim creates strong loyalty. A difficult one creates lasting dissatisfaction. This duality is not unique to Niva Bupa. It exists across the industry. But it highlights one truth. In insurance, perception is built not over years, but in a few critical moments.

10. Challenges and Risks in the Business

10.1 Regulatory Challenges

Insurance is one of the most tightly regulated sectors in India. Companies like Niva Bupa Health Insurance must follow strict guidelines set by regulators. These rules cover everything from pricing to claim settlements. Compliance is not optional. It is fundamental to survival. For customers, regulation offers protection. It ensures that insurers cannot act arbitrarily. For companies, however, it adds complexity. Every new rule requires adjustments in processes, pricing, and product design. This constant balancing act between innovation and compliance is one of the biggest challenges in the industry.

10.2 Operational Risks

Running a health insurance business is far more complex than it appears. Every claim must be evaluated carefully. It involves medical reports, hospital coordination, and policy interpretation. Even a small error can have large consequences. A wrongly processed claim can lead to financial loss for the company or dissatisfaction for the customer. There is also the challenge of scale. As the number of policyholders grows, so does the volume of claims. Managing this without compromising quality is difficult. From a customer’s perspective, these operational challenges are invisible until something goes wrong. But when they do, they directly impact trust.

10.3 Market Competition

The health insurance market in India is intensely competitive. New players are entering with aggressive pricing and innovative features. Existing companies are improving their offerings to retain customers. In this environment, standing still is not an option. Niva Bupa must continuously evolve. It needs to improve its products, refine its claims process, and enhance customer experience. At the same time, it must maintain financial discipline and comply with regulations. This constant pressure defines the business. For customers, competition is beneficial. It leads to better products and services. For companies, it creates a relentless need to adapt, improve, and prove their value again and again.

11. Future Outlook for Niva Bupa and Health Insurance

11.1 Growth Opportunities

The future of health insurance in India is not just promising. It feels inevitable. Every year, medical costs rise faster than most families expect. A single hospitalization can quietly erase years of savings. Because of this, more people are waking up to a simple truth. Health insurance is no longer optional. For Niva Bupa Health Insurance, this shift creates a powerful opportunity. The market is still underpenetrated, especially beyond metro cities. Millions of families remain uninsured or underinsured.

As awareness grows, first-time buyers are entering the system. These customers are not just looking for policies. They are looking for clarity, reassurance, and simplicity. If Niva Bupa can meet that expectation consistently, it stands to gain significantly. But growth will not come automatically. It will depend on how well the company earns trust in moments that truly matter. Because in insurance, growth is not driven by marketing alone. It is driven by how people feel after a claim.

11.2 Digital Transformation

Technology is quietly reshaping the entire insurance experience. What once required physical paperwork, multiple visits, and long waiting periods is now happening on a screen. Policies are bought in minutes. Claims are tracked in real time. Support is just a click away. Niva Bupa has clearly invested in this transformation. Its digital platforms aim to remove friction from every stage of the customer journey.

For a young, tech-savvy customer, this feels natural. Everything is fast, transparent, and accessible. But the real challenge lies deeper. Technology can simplify processes, but it cannot replace trust. A smooth app experience means little if a claim feels delayed or unclear. The future will belong to companies that combine both. Speed and empathy. Automation and human understanding. Digital transformation is not just about tools. It is about creating an experience where customers feel supported, not processed. If Niva Bupa can achieve that balance, it will not just grow. It will lead.

11.3 Long-Term Vision

At its core, the long-term vision for Niva Bupa Health Insurance revolves around one idea. Make healthcare financially accessible without making it emotionally exhausting. Customer-centricity is often used as a buzzword. But in insurance, it has a very real meaning. It shows up in how clearly policies are explained. How quickly claims are handled. How respectfully customers are treated during difficult times. Improving accessibility is not just about expanding hospital networks. It is about making the entire journey easier to understand and navigate. For a first-time buyer, accessibility means clarity. For an existing customer, it means reliability. Family in crisis, it means immediate support.

The companies that succeed in the long run will be the ones that understand these layers. Niva Bupa’s future will depend on how well it continues to align its systems, processes, and people around this single goal. Because in the end, insurance is not about policies. It is about peace of mind.

12. Learning for Startups and Entrepreneurs

The journey of Niva Bupa Health Insurance offers lessons that go far beyond insurance. It reflects how businesses evolve when they operate in emotionally sensitive markets. The first lesson is simple, yet often ignored. Customer focus is not about features. It is about understanding what people feel when they use your product. In healthcare, that feeling is often fear, urgency, and uncertainty. Designing for that reality changes everything. The second lesson is about innovation. Growth does not come from doing the same thing better. It comes from rethinking the experience. Niva Bupa’s shift toward digital platforms shows how traditional industries can reinvent themselves. The third lesson is transparency. Trust is fragile. One unclear clause or one unexpected rejection can damage it. Businesses that communicate openly, even when the message is difficult, build stronger relationships over time.

Finally, adaptability defines survival. Markets change. Customer expectations evolve. Regulations tighten. Companies that resist change fall behind quietly. For entrepreneurs, the takeaway is deeply human. Build systems, but do not forget people. Optimize processes, but do not ignore emotions. Because in the end, businesses do not succeed only because they are efficient. They succeed because they are understood and trusted.

About foundlanes.com

foundlanes.com is India’s leading startup idea discovery platform. It helps entrepreneurs find actionable startup opportunities, market insights, and industry-specific guidance to turn ideas into real businesses. With deep research and practical resources, foundlanes supports founders at every stage, from idea validation to launch and growth.